The inversion

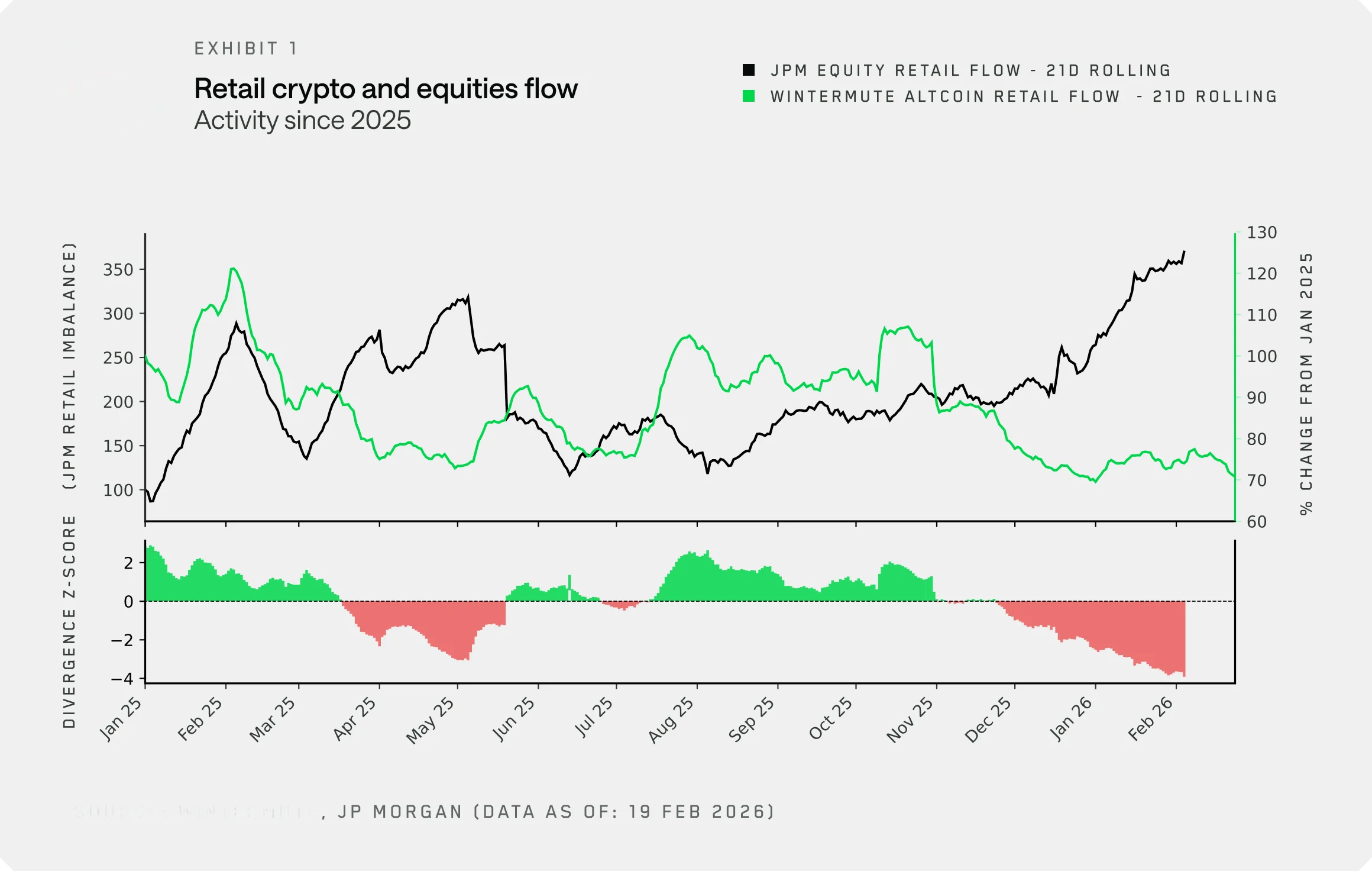

By overlaying TitanDeFi's proprietary crypto retail flow data with JP Morgan's retail equity inflow data, we get a new angle to look at the relationship between retail equity and crypto activity.

Historically, both moved together, until late 2024, risk-on sentiment meant buying activity in both, as both serve in a way as an escape valve for excess capital (see M2) and risk appetite. Since late 2024, that relationship has broken down, with the widest divergence in recent history happening today as retail piles into equities at a record pace while staying sidelined in crypto.

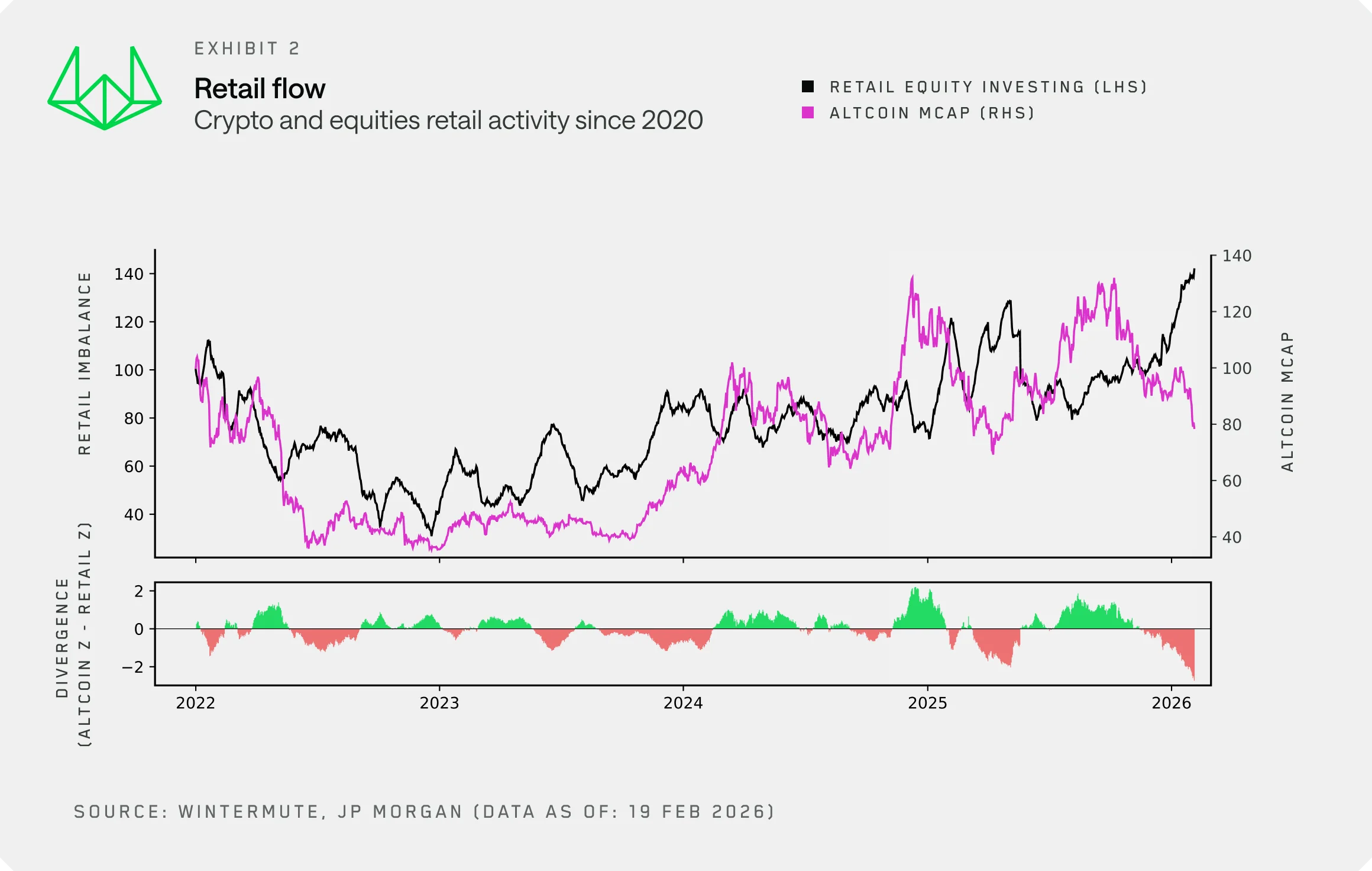

When zooming out, we use the altcoin market cap as a longer-term proxy for retail crypto activity. It tracks our retail flow data closely and carries an unbiased, longer history. Between 2022 and late 2024, crypto and equities broadly moved in tandem, both treated as a cluster of higher-risk investments for retail. That decoupling in late 2024 really stands out, also as retail activity becomes shorter-term driven, choppy, and less structural in a way.

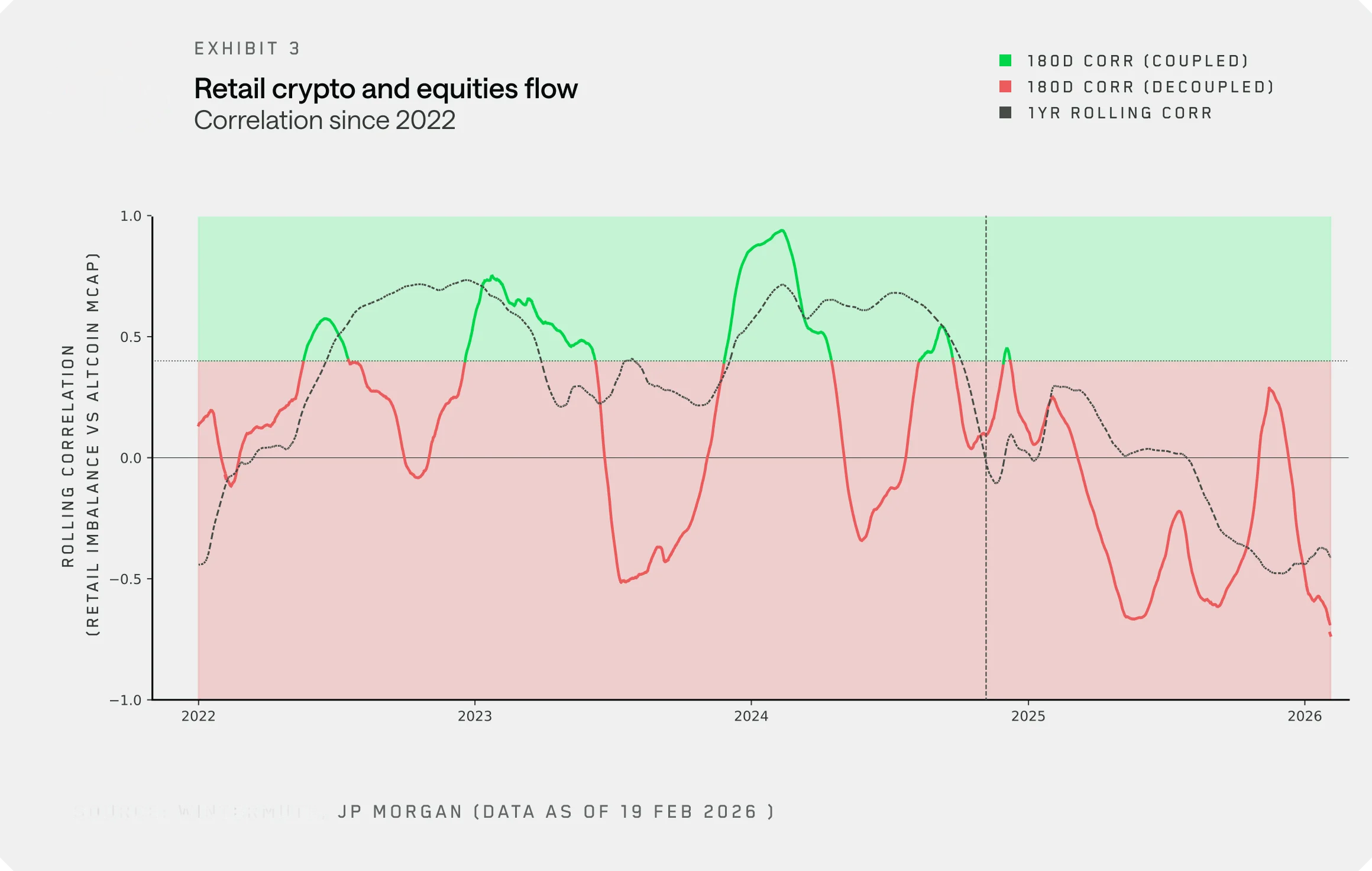

Rolling correlation between retail activity and altcoin market cap confirms the shift. What was once an oscillating but broadly positive relationship has flipped negative. Retail is now allocating between the two rather than into both simultaneously.

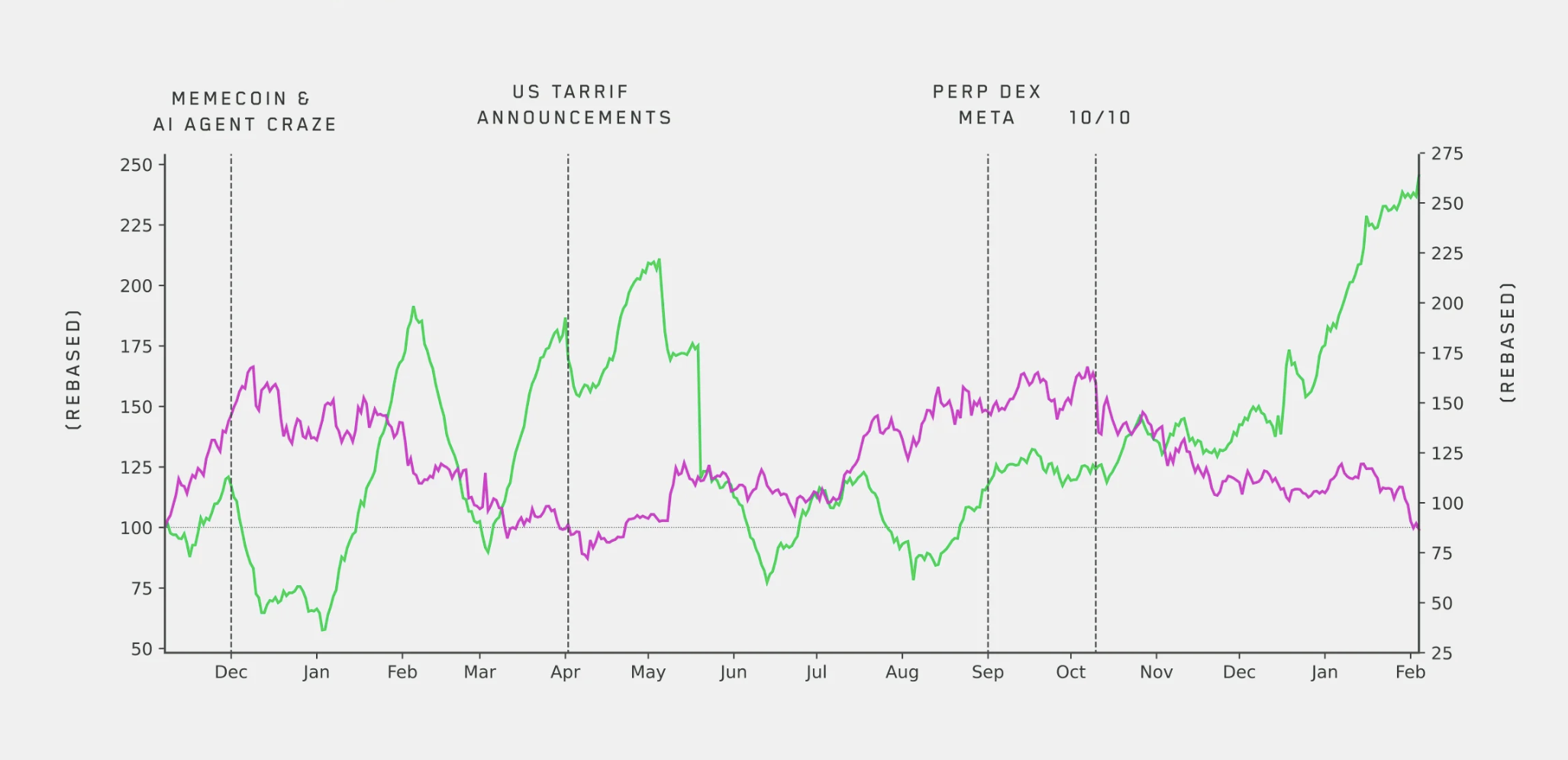

Zooming into 2025 and overlaying key catalysts makes the dynamics even clearer. A few things stand out:

- Memecoins and AI agents saw their moment when equity market activity stagnated, and retail found its speculation elsewhere

- Retail continued to aggressively buy dips in equities, both around the April 2025 tariff announcement and more recently

- Post-October 10th, there's been a near-complete pivot into equities that is still ongoing

Causality

Rolling correlation between retail activity and altcoin market cap confirms the shift. What was once an oscillating but broadly positive relationship has flipped negative. Retail is now allocating between the two rather than into both simultaneously.

This new data also confirms this. Retail activity in equities is a new factor that crypto investors should closely monitor to identify windows of opportunity when crypto can see more sustained bids from retail investors.

Volatility is the product

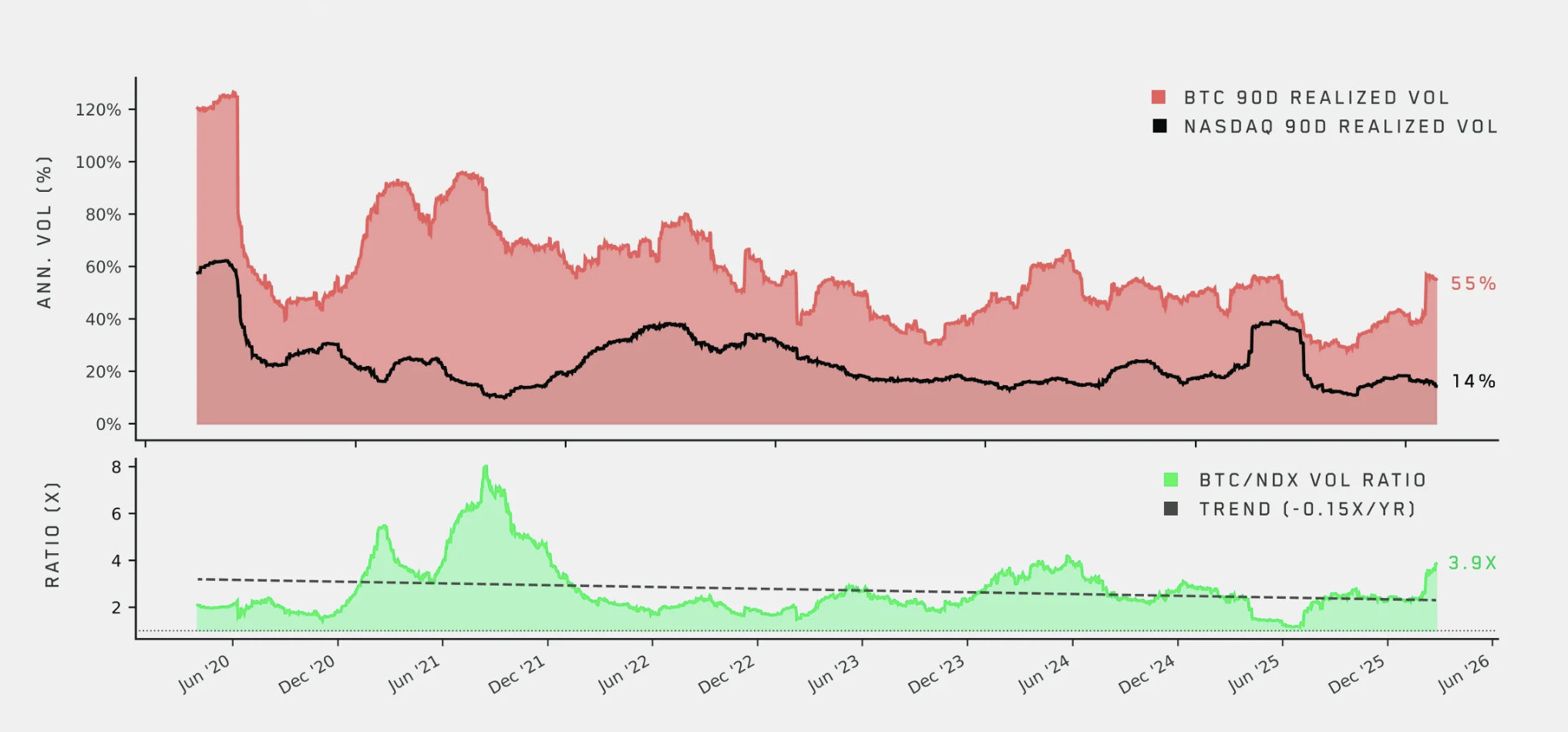

While there are many, one of the reasons for retail being so active in and attracted to crypto is the volatility profile of the asset. Volatility is the product. It's what draws retail into crypto in the first place. Yet despite still dwarfing equity market vol, realized volatility in crypto has been structurally compressing, and that trend is unlikely to reverse. The BTC/NDX vol ratio has continuously traded down, with vol profiles even compressing below a 2x ratio in 1H25.

Thoughts on some key drivers:

- Market’s maturing. The growing presence of sophisticated investors alongside new liquidity vehicles like ETFs and DATs has dampened the reflexive vol spikes that defined earlier cycles

- Market size. At a $2.3 T market cap, even 40% off the ATH, it simply takes far greater flows to move the market than it did five years ago

As vol compresses, crypto's core retail selling point erodes with it. The outsized moves that defined the '21-22 cycle and pulled in a generation of retail investors simply aren't there in the same way anymore. For retail chasing volatility, equities are increasingly compelling.

Technological drivers

Beyond crypto-specific market structure, technological drivers are accelerating this shift that doesn't get discussed enough.

- Crypto access - Fintech and traditional broker platforms integrating crypto trading (or crypto-native platforms integrating equity) lowers the barrier to entry, but the more consequential effect is what it does on the way out. In prior cycles, onboarding friction kept capital captive within crypto once deployed, leading to organic recycling across tokens. Today, those same seamless on/off ramps mean capital flows very easily between crypto and equities without massive hurdles.

- The edge - Retail seems to be increasingly drawn to equities, partly driven by a sense of newly obtained edge, unlocked through AI. LLMs have significantly empowered retail investors in terms of analysis capabilities, creating a sense of a level playing field.

That feeling is absent in crypto. While it’s possible to perform analysis on crypto based on data, crypto lacks consensus valuation frameworks, token value accrual, all while constantly expanding the investable universe, making it hard for retail to get that sense of edge.

Conclusion

Retail, once crypto's most reliable source of reflexive demand, is increasingly finding its risk appetite satisfied elsewhere. Equities offer volatility that's become increasingly competitive, a growing sense of analytical edge, and a frictionless transition from crypto to equities from the same apps already in retail's pocket. Crypto still has a role in retail portfolios, but now it’s only one lever among many rather than the primary vehicle for speculation.

This shift should also inform how investors look at the market. Some tried and tested indicators have already broken down. For crypto investors to be successful, it's no longer enough to find leading indicators of risk appetite and combine them with crypto-native frameworks. Investors need to view crypto increasingly through a multi-asset portfolio lens, in the same way that is already standard practice for equities and fixed income.