Inflation Hot, Oil Down

Macro

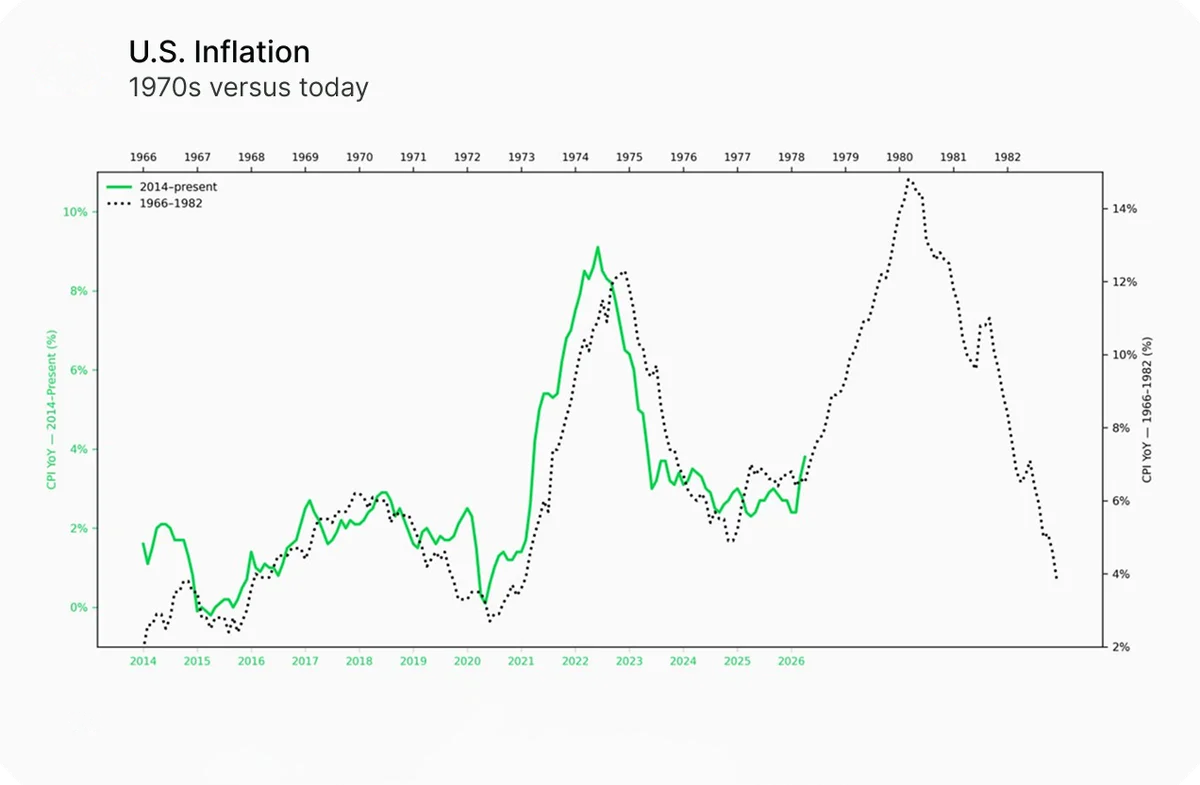

April PCE came in at 3.8% headline and core ticked up to 3.3%. Inflation is still running hot and core is drifting the wrong way.

The better news in oil. Brent fell to ~$91, down 20% on the month, the biggest monthly drop since Covid, on improving Iran rhetoric and a tentative 60-day ceasefire extension. The 10Y eased to 4.45%. Lower oil should pull the headline down over the coming months, so the forward path looks better than the April data.

Reality is that core is the number to watch. If the energy shock has worked its way into services and wages, headline can roll over while core stays sticky. That's the risk we've been flagging since the war: first-round energy relief doesn't necessarily bring the underlying trend down with it, especially with AI demand keeping the economy hot. The bond market gets this. December hike odds peaked above 50% after CPI and have eased back to 35-40% as oil fell, but they haven't gone away. Yields are pricing inflation, not relief. It’s not unthinkable to see “stagflation” and “double dip inflation” pop up again in Q3 as we head into years end.

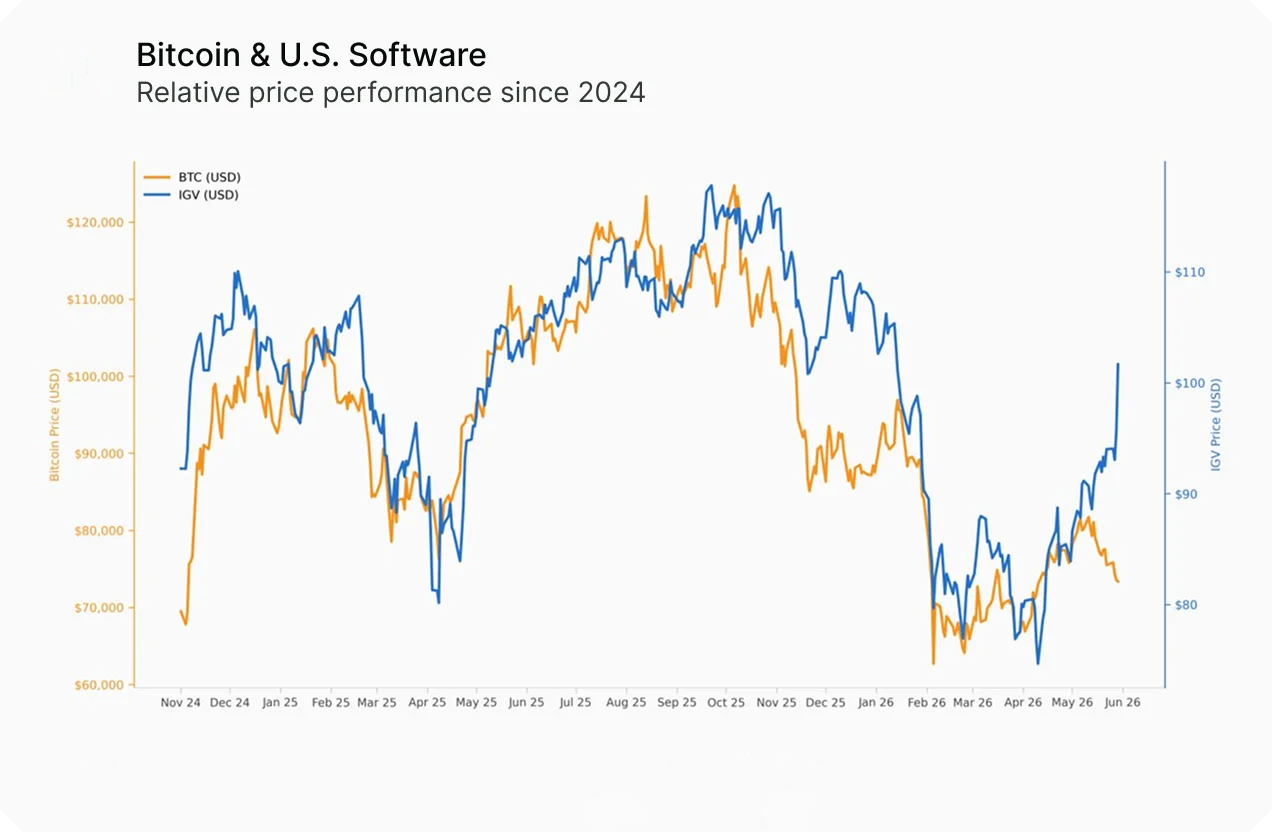

Equities are their own story. The rally is broadening from semis into software, with names like Dell, Snowflake, IBM and Salesforce all delivering on AI earnings. That broadening is the more durable read, because demand is being delivered rather than just promised, and you can see it cleanly in software's outperformance against BTC. S&P +1.9%, 9th straight green week. Nasdaq +8% on the month. Equities aren't rallying because the macro improved. They're rallying because AI earnings keep printing and the market is choosing to look through everything else.

Digital Assets: Testing the Ceiling

BTC closed near $73,500, ETH around $2,000, majors down over 4% on the month while alts were marginally up. Second straight week of crypto sitting out the equity rally, and the cleanest decoupling print this year. The risk-on rotation went into Nasdaq and the Russell 2k. Crypto, the most risk-sensitive cross-asset class, got skipped. Typical bear behaviour, and it's been this way for a while.

The reason is simple. Equities have an earnings story to lean on. Crypto doesn't. So while the Nasdaq looks through a hostile rate backdrop on the back of AI capex, crypto is fully exposed to the macro everyone else is ignoring.

The flow data is the rest of it. BTC spot ETFs lost another ~$1.4B, the longest redemption streak since launch, ETH another ~$240M. May 20-29 alone, BTC and ETH ETFs shed ~$2B combined while XRP took in $35M. The bid that carried BTC from $70k to $80k in April is gone. And as of writing, Strategy is selling, which is feeding the bearish tone among the crypto-native crowd.

Underneath, the longer-term picture is more constructive than price suggests. While there's still some debate over whether we're in a bear market or not, to us it looks like the cycle is resetting. The setup looks relatively weak into the summer months, but we're seeing longer-term holders start to TWAP into the market through the OTC desk, with no appetite to call the exact bottom but a view that these levels look attractive on an 18-month basis.

HYPE is the only thing on the alt side that matters, crossing $70 today. Grayscale negotiated a ~$115M seed for its HYPE ETF, ICE's Sprecher name-checking Hyperliquid at Bernstein. HYPE has decoupled from the market since the start of the year, the hallmark of a major token forming.Beyond HYPE, the rally is selective: privacy, AI and perps, in a very narrow fashion. The common denominator across all of them is a focus on applications and platforms rather than pure infrastructure, which was what led the past two alt rallies. If (d)apps really are the winners of the next cycle, we'll likely see a shakeup in the constituents of the top 50-100 tokens.

Our take:

“Equity rally broadens while crypto lags"

Equities rallied this week, but not because the macro got better. Core PCE ticked up, the 10Y is at 4.45%, and the market still prices 35-40% odds of a hike this year. The bond market is starting to think the Fed is behind the curve on inflation. Equities are climbing through that on the AI earnings story. Crypto has no equivalent, so it's left holding the macro everyone else is ignoring.

$2B out of BTC and ETH ETFs in 10 days, the longest redemption streak since launch, and now Strategy selling. The marginal dollar that was in crypto in April is in Nvidia, Dell and small caps. When the headwind eases and crypto still can't catch a bid, the problem isn't macro, it's that there's no marginal buyer.

The software/BTC correlation has snapped, retail is still in equities, and there hasn't been enough capitulation to call a clean bottom. The one thing to watch is ETF flows flipping back to sustained inflows. That marked the institutional return in April, and its absence is what's keeping spot heavy.

~$72k is where we are, low 60s underneath. CPI/PPI Wednesday and the CME Nasdaq crypto index futures launch Monday are the near-term catalysts. It's also worth keeping an eye on what tokens HYPE's gains recycle into. We saw this with BNB last year, where if they perform, the spillover can be meaningful.